The Greek Debt Crisis

✍ By Sarthak Jain | 🌍 India | 📅 Thu Oct 23 2025

The Greek Debt Crisis

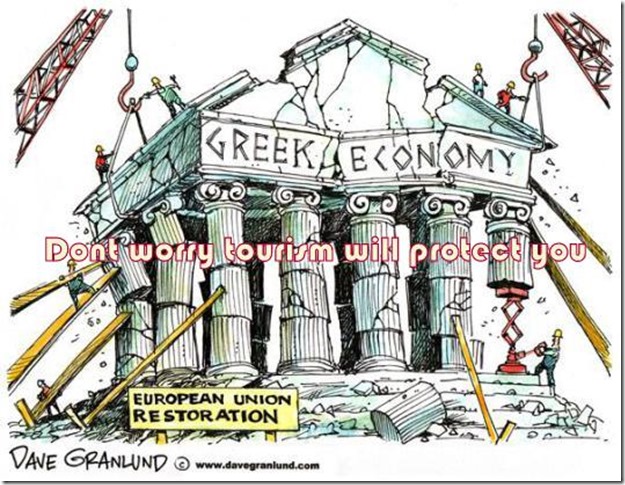

Greek debt crisis, which unfolded over the last decade, challenged the conventional assumption that advanced economies can never default and are, in financial jargon, AAA rated. It is the perfect example of the fragile balance between trust, policy and market forces. Greece was one of the best performing economies in the European bloc. It had high GDP growth fueled by a booming tourism and shipping industry due to its position in the Mediterranean region. It was classified as a mixed advanced economy. However, there were underreported fiscal and trade deficits. As we can see there are some underlying problems. Firstly, being an advanced economy, it had high GDP per capita which in turned caused its labor to be expensive with respect to other countries. Secondly, tourism and shipping are not very stable sources of revenue. Lastly, Greek government was fiscally very inefficient. A major part of the government spending went to military which produced no tangible effects on the economy and the GDP. Then the Global Financial Crisis happened in 2008. This sent the western world into a recession. Tourism in Greece nose-dived. And since the western world was reeling from the series of failing companies, trade and shipping was also hit. Hence, Greek GDP started to fall. Usually in such a scenario of falling GDP, countries devalue their currency to boost their exports and stabilize the GDP growth. However, in this case Euro was controlled by all the European countries who did not want to devalue it as imports would become expensive. So, Greece had no choice but to increase borrowing to keep running the country. The fiscal and trade deficit grew 3 times from below 5 percent of GDP in 1999 to 15 percent in 2008-9. However, these numbers were underreported by the Hellenic Statistical Institute. Finally, EU’s Excessive Deficit Procedure revised the deficits and the final debt to GDP stood at 115%. After this startling report, the bond yields spiked as investors started to sell off the Greek bonds with Moody’s changing the Greek bond status to junk. Spike in yields made it harder for the government to repay these debts. Moreover, the nominal GDP growth was not enough to maintain the debt level. To repay these debts, major banks like Goldman Sachs restructure these loans into complex financial derivatives along with currency swaps. In 2011, private bond investors had to accept a cut in their bond repayments which reduced investor confidence a lot as sovereign bonds were seen as the gold standard which never lost value. Greece received multiple bailouts from the European Central Bank and IMF which caused it to accept austerity measures which crumbled the economy with large scale job losses and an overall recession. In 2019, Greece issued 10-year bonds again for the first time post-crisis. But GDP had still not recovered to pre-2008 levels even after a decade. At its core, the Greek debt crisis was not just about numbers or markets — it was a crisis of structure and trust. Despite being an advanced mixed economy, Greece lacked stable and scalable sources of income, making meaningful cuts to government spending politically and economically difficult. But perhaps the most damaging blow came from the erosion of trust — when economic data was misreported and deficits were masked, investors lost faith. And in finance, once trust breaks, recovery becomes a long uphill climb.

📖 More Articles

Jabong’s Fade-Out: A Cautionary Tale in Indian E-commerce

✍ Sarthak Jain

Story of Takeoff to Turbulence

✍ Sarthak Jain

CCD’s Quiet Retreat

✍ Sarthak Jain

Why Dazo Couldn’t Scale: A Case Study in Food-Tech Fragility

✍ Sarthak Jain⭐ Reviews

✨ Be the first one to add a review!